How Mutual Funds Work in 2026: Simple Guide for Beginners

How Mutual Funds Work: A Simple Guide for 2026 (Stop Guessing, Start Investing)

Let’s be real for a moment. The stock market can be absolutely terrifying—especially if you’re just entering the world of investing. You open a chart, and suddenly you’re lost in a jungle of squiggly lines, red candles, green candles, global news alerts, and headlines about a crash in Japan. At that point, keeping your money tucked under the mattress almost feels like a wise, peaceful life decision.

But you also know the truth: Inflation is your silent enemy. Your money is losing value every year if it just sits around doing nothing.

You need to invest. And this is exactly where Mutual Funds step in—simple, structured, and investor-friendly.

Mutual funds are the bridge between “saving money” and “building wealth”… and the best part? You don’t need to be a full-time stock market genius to use them.

In this detailed 2026 guide, we’re stripping away the financial jargon. You’ll learn:

- How mutual funds work

- How mutual fund returns are calculated

- Are mutual funds safe or risky?

- How mutual funds are taxed

Let’s dive in.

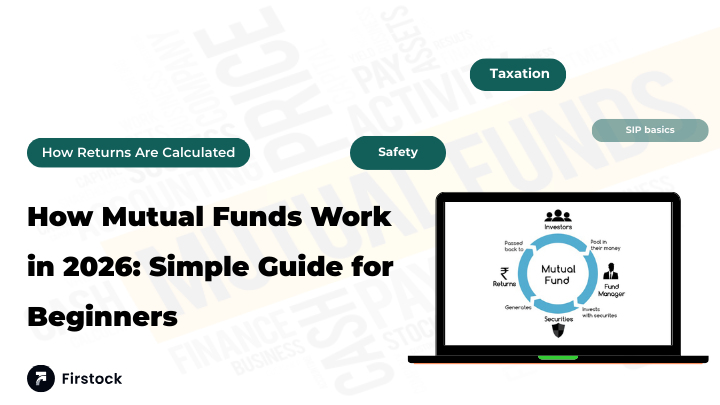

What Is a Mutual Fund? (The Famous “Bus Analogy”)

If you search “how mutual funds work” online, you’ll find complicated definitions. But here’s the simplest one:

Picture a bus. You’re one of the passengers. You want to reach a destination—let’s call it wealth.

Maybe you don’t have a car… or maybe you just hate driving in traffic. So, you and a bunch of other people buy tickets. These tickets represent your investment.

All of you together hire a bus. But someone has to drive the thing, right?

That driver is the Fund Manager.

This person:

- Knows every shortcut

- Understands the road

- Avoids potholes

- Chooses the safest and smartest route

You simply pay a small fee and enjoy the ride.

That’s the story of a mutual fund:

A bunch of investors pooling money → A professional manager investing it → Everyone sharing the profits.

The fund invests your money across several assets like:

- Stocks

- Bonds

- Government securities

- Gold (in certain funds)

The Mechanics: How Mutual Funds Actually Work

When you invest ₹5,000 in a mutual fund, you’re not buying a specific stock like Reliance or Tata Motors. You’re buying Units of the fund.

Here’s how the entire system works step-by-step:

1. The Pool: Collecting Money

The mutual fund company (AMC) collects money from millions of people.

Example: Let’s say they gather ₹100 Crores.

All this money is pooled into one giant basket.

2. The Allocation: Diversification

The Fund Manager then invests this pooled amount into around 50 different companies (or bonds, depending on the type of fund).

This is called diversification.

Why is this important? Because if one company fails badly… You don’t lose everything.

Your risk is spread across multiple high-quality companies.

3. The NAV (Net Asset Value): Your Unit Price

This is the price of one unit of the mutual fund.

If the value of the underlying stocks goes up → NAV increases If the market crashes → NAV decreases

That’s it. Simple and clean.

How Mutual Funds Work

A mutual fund works by pooling money from many investors and investing it into diversified assets like stocks or bonds. You buy “units” of the fund at a price called NAV. A fund manager handles the investments, and your returns depend on how these assets perform.

How Mutual Funds Returns Are Calculated

If you bought a stock at ₹100 and sold it at ₹120, your profit calculation is easy: 20% return.

But mutual funds are different because:

- You may invest monthly (SIP)

- NAV changes every day

- You buy units at different prices

- You redeem at a different NAV

So how do you calculate mutual fund returns correctly?

Let’s break it down.

1. CAGR (Compound Annual Growth Rate)

This is the most common and widely used method.

CAGR helps you understand the average annual growth of your investment over time.

If you invested a lump sum ₹1 lakh five years ago, CAGR tells you the consistent yearly growth rate that takes your investment from point A to point B.

Investors love it because: ✔ It smooths out volatility ✔ It gives a realistic picture ✔ It’s easy to compare across funds

2. XIRR (Extended Internal Rate of Return)

This is the king of SIP returns.

Why? Because in SIP, you’re investing monthly. Sometimes:

- NAV is high

- NAV is low

- You buy more units when the market dips

- You buy fewer when it rises

A simple percentage calculation fails here. That’s where XIRR shines—it calculates returns on each SIP installment and gives your true total return.

Pro Tip: Use the Firstock - Trading App for beginners to track your XIRR automatically. It does all the complex math for you instantly.

How Mutual Fund Returns Are Calculated

Mutual fund returns are mainly calculated using CAGR for lump-sum investments and XIRR for SIPs. CAGR measures the average annual growth rate, while XIRR calculates returns across multiple investments made at different times and NAVs.

Are Mutual Funds Safe?

This is the most common question beginners ask.

Here’s the honest truth:

No investment in the world is 100% safe. Not even your savings account (because of inflation).

But mutual funds are significantly safer than picking random stocks based on “gut feeling.”

Why? Because of:

- Diversification

- Professional management

- Strict regulations

Let’s understand the risk side too.

The Risks You Should Know

1. Market Risk (Equity Funds)

If the stock market falls, your equity mutual fund will fall.

That’s the game. No sugarcoating.

2. Credit Risk (Debt Funds)

If a company fails to repay its debt (rare, but possible), your debt fund can take a hit.

The Safety Nets That Protect You

✔ SEBI Regulation

Mutual funds are tightly regulated. Fund houses cannot run away with your money.

✔ Transparency

Every month, you get a detailed fact sheet showing exactly where your money is invested.

✔ Professional Fund Managers

You have experts watching the market for you.

Are Mutual Funds Safe?

Mutual funds are not completely risk-free, but they are safer than directly picking stocks because they offer diversification, SEBI regulation, transparency, and professional management.

How Mutual Funds Are Taxed in India (2026 Guide)

No one likes taxes. But understanding how mutual funds are taxed is absolutely necessary.

Taxation depends on:

- Type of Fund (Equity vs Debt)

- Holding Period

Let’s break it down simply.

Equity Funds (Invested in Stocks)

Short-Term Capital Gains (STCG)

If you sell within 1 year → Flat 20% tax

Long-Term Capital Gains (LTCG)

If held for more than 1 year:

- Profits above ₹1.25 Lakhs in a financial year → 12.5% tax

- Profits below ₹1.25 Lakhs → Zero tax

Debt Funds

These follow your income tax slab.

If you’re in the 30% slab, you pay 30% on your gains.

Simple.

How Mutual Funds Are Taxed

Equity mutual funds are taxed at 20% for short-term gains and 12.5% on long-term gains above ₹1.25 Lakhs. Debt mutual fund gains are taxed according to your income tax slab.

Conclusion: Stop Guessing, Start Investing

Mutual funds are the democratization of wealth. They allow you to own a piece of India’s biggest companies with as little as ₹500.

You don’t need to be a market expert. You only need to be consistent.

Understanding how mutual funds work is step one. Step two is execution.

And with stock trading apps like Firstock, investing in Direct Mutual Funds is no longer a complicated process.

Just:

- Log in

- Pick your fund

- Start your SIP

- Let compounding handle the rest

FAQs

1. Can I lose all my money in a mutual fund?

In a diversified fund, the chance of losing everything is extremely rare. You’re investing in India’s top companies—not gambling on one single business.

2. What is a "Direct" Mutual Fund?

Regular plans charge broker commissions. Direct plans do not, so your returns are higher.

Firstock offers Direct Mutual Funds.

3. How do I withdraw my money?

Simply place a redemption request in your trading app. Money usually comes within 1–3 days.

4. What is the best mutual fund for beginners?

Two great beginner-friendly choices:

- Nifty 50 Index Fund

- Flexi-Cap Fund

They offer broad exposure without complexity.

5. How does a SIP work?

A SIP automatically invests a fixed amount monthly. When the market dips, you buy more units. When it rises, you buy fewer.

This makes wealth creation smooth and disciplined.

6. How much should a beginner invest in mutual funds?

Start with whatever amount you’re comfortable with—even ₹500 is enough. Consistency matters more than size.

7. Can mutual funds make you rich?

Yes, but slowly and steadily. Mutual funds are long-term compounding machines, not quick-profit schemes.

8. Which is better: SIP or lump-sum?

- SIP = Best for salaried individuals & volatile markets

- Lump-sum = Best during market corrections if you have spare cash

9. How long should I stay invested in mutual funds?

Ideally 5–10 years. The longer you stay, the stronger compounding becomes.

10. Do mutual funds have hidden charges?

No hidden charges. All expenses are clearly listed in the Expense Ratio.

Disclaimer

Investments in the securities market are subject to market risks. Read all related documents carefully before investing. This blog is for educational purposes only.